skynesher

The US economy is likely to slip into a recession by the end of 2024, and thus the S&P 500 is on the verge of a recessionary bear market.

Why a Recession?

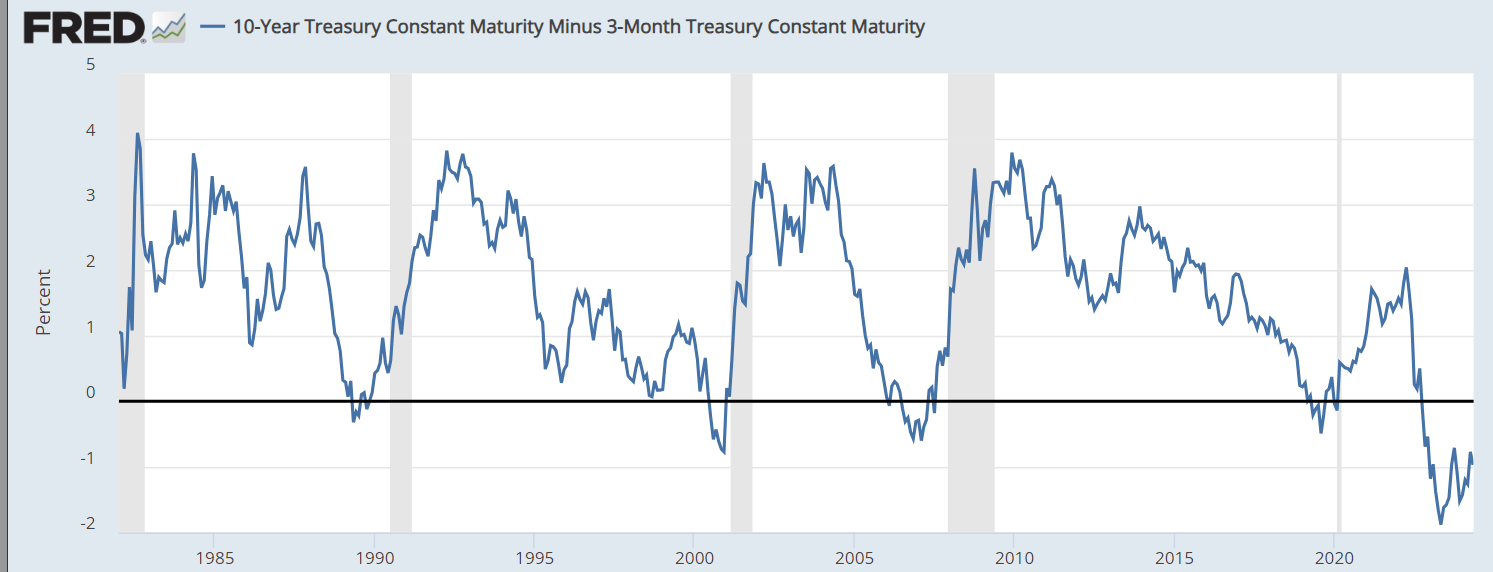

The Fed was forced to hike interest rates in 2022/2023 from 0-0.25% to 5.25-5.50% in response to the rising inflationary pressures. As a result, the yield curve inverted, as the short-term interest rates exceeded the long-term interest rates.

The inverted yield curve causes a recession – that’s based on historical evidence. Specifically, the yield curve inverts the credit availability tightness, which causes less investment, and ultimately higher unemployment rate.

However, the effects of monetary policy tightening affect the real economy with long and variable lags, and it could take 12-18 months from the initial inversion until the economic data starts turning negative.

In addition, the evidence indicates that the longer the yield curve stays inverted and the deeper the inversion, the longer and the deeper the resulting recession.

Currently, the difference between the 10Y Treasury Note yields and the 3M Treasury Bill yield is negative, so the yield curve is inverted, and it has been inverted since October 2022 – and this is the longest inversion on record (since 1980). In addition, the inversion level has reached the deepest point ever at -1.9%. Thus, the upcoming recession is likely to be much deeper and longer than the average, based on historical evidence.

So, why is the yield curve inverted? The yield curve is inverted because the Fed needs to create a recession to restore price stability. That’s a normal business cycle.

{kind=link}

Why is it Taking So Long?

The yield curve has been inverted since October 2022, that’s for about 18-19 months already, and the US economy is still growing. Why does it take so long for the monetary policy tightening to affect the economy during the recent cycle?

The US economy has proven to be resilient and defied the recessionary expectations, but this is due to these temporary pandemic-related events: excess pandemic savings, boost in immigration, and fiscal spending.

Excess pandemic savings

First, after the extraordinary pandemic-related stimulus, the consumer accumulated $2.1 trillion in excess savings, and once the economy reopened the consumer went on a revenge spending binge, which kept the economy growing in 2023 and delayed the recession. However, those excess savings are now completely gone. As a result, it is likely that discretionary consumption will decrease and contribute to the recessionary pressures.

Increase in immigration

There was a sharp increase in immigration to the US in 2023, as evident in the increase in foreign-born workers. The resulting increase in labor force boosted the supply of workers, which helped reduce the labor shortage and thus wage growth, and also increased the overall consumption, which boosted economic growth and delayed the recession.

However, the boost in (legal) immigration in 2023 was mostly due to the large backlog in USCIS visa processing due to the pandemic. In 2023, USCIS processed over 10 million applications, and reduced the backlog by 15%.

Fiscal spending

The US government continued to stimulate the economy with the pandemic and pandemic-related stimulus even in 2023 and 2024, with the federal deficit at -6% of GDP, and debt at 121% of GDP. This pro-cyclical government spending counters the monetary policy tightening measures.

The Soft-Landing Hopes

In addition to the defiant growth in the US economy in 2023, inflation also continued to fall faster than expected. But this was also due to the temporary pandemic-related variables. Specifically, the goods prices fell faster than expected as the post-pandemic supply chain bottlenecks eased.

The Fed noticed that inflation was falling faster than expected, and suggested that it might be possible to reduce (normalize) interest rates before the recession hits. Thus, the Fed made an official dovish turn in December 2023, signaling the beginning of policy normalization, while assuming no increase in the unemployment rate – thus, no recession.

The policy rate normalization means that the Fed would lower the short-term interest rates below the long-term interest rate, and create a “normal” steep yield curve – all before the recession hits.

However, the subsequent easing of financial market conditions, as interest rates fell, caused a resurgence in inflation during the first quarter of 2024. Thus, the Fed gradually walked back the pre-mature normalization plans, and signaled the return of the “higher-for-longer policy”, which essentially means “higher until recession”.

The Fed is now aware that it would be impossible to normalize interest rates with full employment, as this causes higher service inflation, and makes it impossible to reach the 2% inflation target. Thus, a recession is needed to restore price stability – and this is a normal business cycle.

Implications

SPDR® S&P 500 ETF Trust (NYSEARCA:SPY) is the most popular ETF that tracks the S&P 500. I rated SPY as a Buy in December, acknowledging the Fed’s normalization plans.

Specifically, my 2024 outlook for SPY was “pump and dump”, where I expected that the underlying S&P 500 index would reach the 5300 level by June, but then the second half of the year would be more difficult as the disinflationary process ends.

However, after the resurgent inflation in January/February and when the Fed started to walk back the normalization plans, I downgraded SPY to a Hold in February, stating that “SPY is currently influenced by the GenAI theme, ignoring the broad market conditions, which is unsustainable“.

Three months after, the GenAI theme is slowly fading out, as the Nasdaq 100 (QQQ) has been underperforming, while the S&P 500 is climbing out of a 5% dip based on the same soft-landing hopes.

However, now we are getting the early signs of a recession. The April payroll report was weaker than expected, the ISM service for April dipped in the contraction territory below 50, and even the initial claims started to rise, spiking to 231K on May 9th.

Yet, the S&P 500 is still climbing based on the hopes that the Fed would start cutting interest rates and cancel the recession – the soft-landing hopes. First, it could already be too late to prevent a recession, even if the Fed cuts, as the excess savings are gone. Second, inflation is still too high, and the ISM Service report confirmed the Q1 GDP report, where growth is slowing, but inflation is rising. Thus, the Fed might not be able to cut, despite the deteriorating economy.

The S&P 500 is still not pricing a recessionary bear market. In a recession, earnings decrease, possibly by 20%. Currently, analysts expect around 10% earnings growth for the S&P 500 – not realistic. Additionally, the PE multiple contracts in a recession to around 15 or below. Currently, the S&P 500 PE ratio is around 22, which is overvalued by historical standards. Thus, the upcoming recessionary bear market will be deep, as the PE multiple contracts, and earnings are revised much lower.

Thus, I am downgrading SPY to a Sell. The top could continue to form as the market continues to price a soft landing, where a “bad news is good news”, but eventually a “bad news will be bad news”.

The SPY Sector Analysis

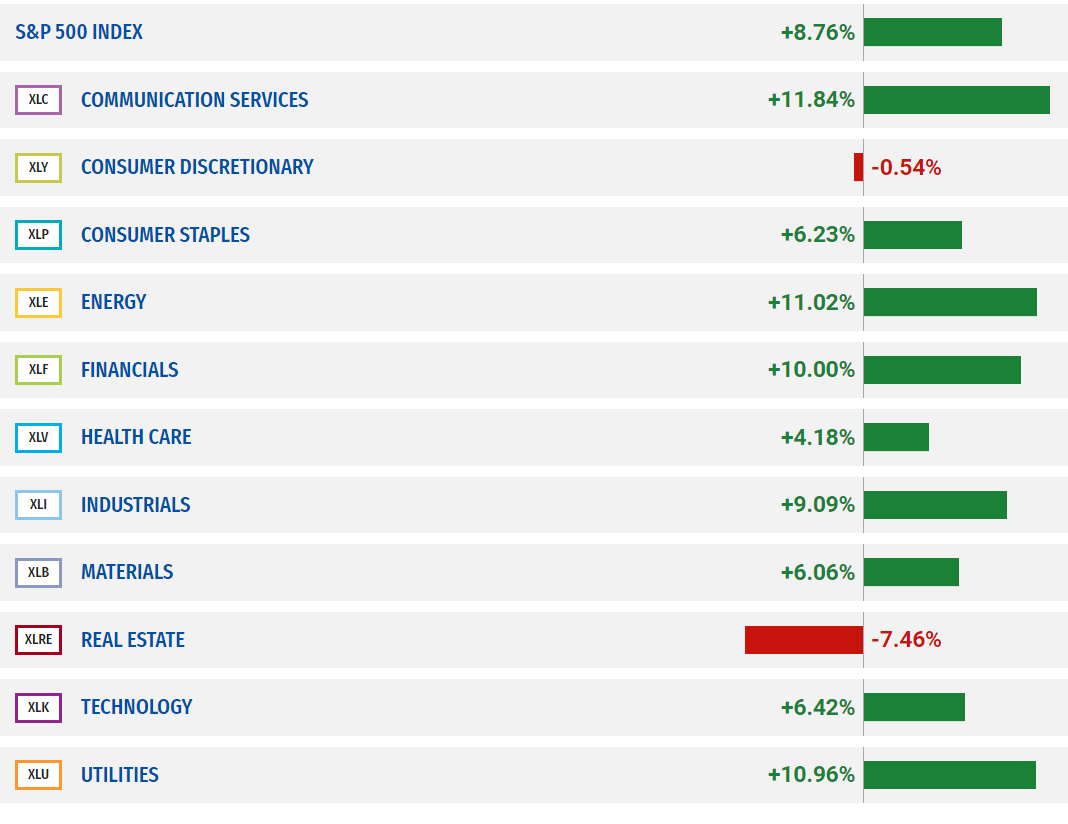

The SPY is up by nearly 9% YTD, and there has been a broadening of the rally beyond the mega-cap tech stocks and the AI theme. Beyond the AI-themed Meta (META) and Alphabet (GOOGL) in the Communication sector (XLC), the rally has been led by Energy (XLE) and Utilities (XLU), as well as insurance stocks in the Financial sector (XLF). These are either inflation-hedge investments or defensive investments, which don’t bode well for the broad market.

On the downside, the Discretionary sector (XLY) is down for the year, where key consumer barometer stocks like Starbucks (SBUX), McDonald’s (MCD), and Nike (NKE) all underperformed. This confirms the early recessionary signals, based on consumption slowdown as excess savings evaporated.

The Real Estate sector (XLRE) continues to underperform, and this reflects continuous worries about an imminent crisis in the commercial real estate CRE market.

{kind=link}

The Sell Rating

This is not a timing call, as the market is still pricing a soft landing, so the uptrend can continue. However, since this is my quarterly report on SPY, I expect that the top will be in place by September, as we get more evidence of a recession.

Read More: SPY: Get Ready For A Recessionary Bear Market (NYSEARCA:SPY)